TL;DR:

- A business’s value is a dynamic estimate influenced by purpose, metrics, and market conditions, not a fixed figure. Calculating enterprise and equity value, along with customer LTV and CAC ratios, provides essential insights for growth and investment decisions. Regularly reviewing these metrics helps owners understand performance, optimize marketing, and prepare effectively for sale or funding.

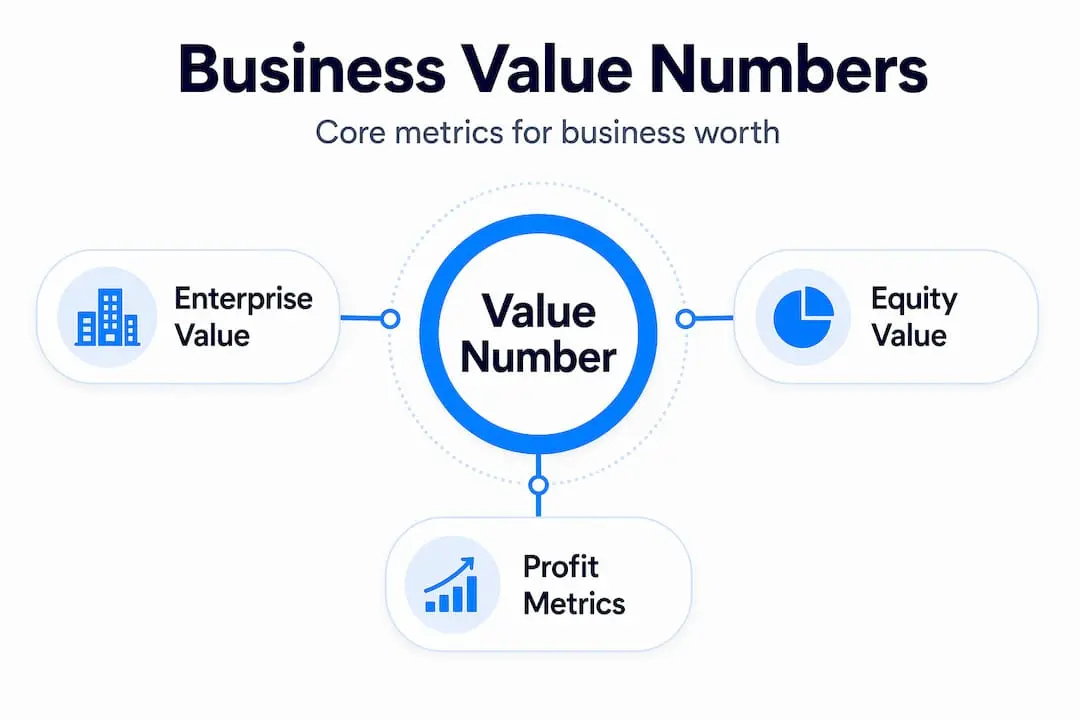

Every business owner wants to know what their company is worth. But ask three different advisers and you will likely get three different answers. That is because a “value number” is not a single fixed figure sitting in a spreadsheet. It is a dynamic estimate that changes depending on your purpose, your industry, and the metrics you choose to measure. Understanding what is a value number for business means grasping several interconnected concepts, from enterprise value and profit multiples to customer acquisition costs and lifetime value. Get these right, and you have a genuine compass for growth.

Table of Contents

- Key takeaways

- What is a value number for business?

- Customer acquisition metrics as value numbers

- How to calculate your business value internally

- Comparing key value numbers and what they reveal

- Putting value numbers to work

- My take on value numbers in practice

- Boost your business value with the right number

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Value is not one number | Business value is a range-based estimate that shifts with purpose, method, and market conditions. |

| Enterprise vs equity value | Enterprise value reflects total operational worth; equity value is what you actually pocket after debt. |

| LTV:CAC ratio matters | A healthy ratio of 3:1 signals sustainable acquisition; below 1:1 means you are spending more than you earn. |

| Internal estimates are useful | You can calculate business value to within 20–30% accuracy without hiring a formal appraiser. |

| Balanced metrics beat one number | Relying on revenue alone misleads; combining enterprise value, LTV, and CAC gives a clearer picture. |

What is a value number for business?

Most owners reach for revenue when someone asks what their business is worth. It is the most visible figure. But revenue alone misleads because it ignores debt, expenses, owner-specific perks, and one-off windfalls. A proper value number considers all of those.

There are two core figures you need to understand: enterprise value and equity value. Enterprise value represents the operational worth of the business independent of how it is financed. It is what a buyer would pay for the entire operation. Equity value is what remains after you subtract outstanding debt and add back any surplus cash. If your business has an enterprise value of £1.2m but carries £200,000 in debt, your equity value is closer to £1m. That distinction matters enormously when you are preparing for investment or a sale.

Common business valuation methods

There are four approaches used in practice, each suited to different circumstances.

Asset-based valuation adds up the net value of everything the business owns minus what it owes. It tends to undervalue businesses with strong recurring revenue or brand equity, so it works best for asset-heavy companies like manufacturers.

Market multiples compare your business to similar ones that have recently sold. Revenue multiples for private businesses range from 0.5x to 5x depending on industry and growth trajectory. A SaaS business with 80% gross margins and 30% year-on-year growth commands a very different multiple than a local services firm with flat revenue.

Profit-based approaches, such as EBITDA multiples, are widely used and give buyers a clearer picture of cash generation. If you want to understand how EBITDA compares to net income as a valuation input, the distinction can shift your final number significantly.

Discounted cash flow (DCF) projects future earnings and discounts them back to present value. It is the most technically rigorous method, but its output is highly sensitive to the assumptions you feed in.

Pro Tip: Adjustments matter as much as the method itself. Owner-driven expenses, generous salaries drawn beyond market rate, and non-recurring items can create a 20–30% valuation discrepancy if left uncorrected. Always normalise these before running any calculation.

| Valuation method | Best suited for | Main limitation |

|---|---|---|

| Asset-based | Asset-heavy businesses | Undervalues intangibles |

| Market multiples | Most SMEs | Comparable data can be scarce |

| Profit-based (EBITDA) | Established profitable firms | Ignores future growth potential |

| Discounted cash flow | Growth-stage businesses | Highly assumption-dependent |

Customer acquisition metrics as value numbers

If you run a growth-focused business, your most telling value numbers are not in your balance sheet. They are your customer lifetime value (LTV) and your customer acquisition cost (CAC). These two figures, and their ratio, tell you whether your growth engine is actually sustainable.

LTV is the total profit a customer generates over their relationship with you. The critical word there is profit. LTV calculated on gross profit margin gives a far more accurate picture than LTV based on gross revenue. Consider this: a customer spending £200 at a 15% margin contributes £30 to the business. A customer spending £150 at a 50% margin contributes £75. The second customer is worth more than twice as much, despite paying less.

CAC is what you spend to acquire each new customer. The mistake most owners make is equating CAC with ad spend. True CAC includes all acquisition costs: salaries for your sales team, agency fees, software subscriptions, content production, and even discounts or promotions used to close deals. Undercount any of these and your acquisition economics look artificially healthy.

Here is why the LTV:CAC ratio is the value number that really drives decisions:

- A 3:1 ratio is the standard benchmark for 2026. You earn £3 for every £1 you spend acquiring a customer.

- A ratio below 1:1 means you are actively losing money on each new customer, regardless of how fast you are growing.

- A ratio above 5:1 often signals underinvestment. You could be acquiring more customers and scaling faster, but you are holding back.

- CAC has risen approximately 60% over the past five years, which means businesses relying on old benchmarks are likely underestimating their true acquisition costs.

- Channel-specific CAC is equally telling. Knowing which channels produce the lowest CAC with the highest LTV allows you to allocate budget with precision rather than guesswork.

Pro Tip: Calculate CAC separately for each acquisition channel every quarter. A channel with a poor blended CAC might still contain one or two highly efficient segments worth scaling.

How to calculate your business value internally

You do not need a formal appraisal to get a useful working figure. Internal valuations can reach within 20–30% of a professional appraisal when done carefully. That level of accuracy is more than sufficient for planning, funding conversations, and spotting equity gaps.

Follow these steps to build a working estimate:

- Normalise your earnings. Start with net profit and add back owner compensation above market rate, personal expenses run through the business, one-off costs such as legal disputes, and depreciation. The resulting figure is your adjusted EBITDA.

- Apply an industry multiple. Research what businesses in your sector are selling for as a multiple of adjusted EBITDA or revenue. Use multiple sources and treat the range as a guide, not a guarantee.

- Calculate enterprise value. Multiply your adjusted EBITDA by the relevant multiple. This is your enterprise value.

- Arrive at equity value. Subtract total debt and add surplus cash. The figure you are left with represents what you would actually receive in a clean sale.

- Calculate LTV with margins. Identify your average customer revenue per year, multiply by your gross profit margin, then multiply by average customer lifespan in years.

- Calculate true CAC. Add up all sales and marketing costs for a period, then divide by the number of new customers acquired in that same period. Include salaries, tools, and agency fees.

- Compare LTV to CAC. Divide LTV by CAC to get your ratio. If it sits below 3:1, investigate which cost drivers are pulling the ratio down.

Understanding how your business is actually performing financially alongside these calculations gives you a three-dimensional view that pure revenue reporting simply cannot provide.

Comparing key value numbers and what they reveal

Different value numbers answer different questions. Knowing which metric to reach for in a given situation prevents the kind of tunnel vision that leads to poor decisions.

| Value number | What it measures | Best used for |

|---|---|---|

| Revenue | Top-line sales performance | Year-on-year growth tracking |

| Adjusted EBITDA | Core profit-generating ability | Valuation multiples and investor conversations |

| Enterprise value | Total operational worth | Acquisition, sale, or fundraising scenarios |

| LTV | Profit generated per customer | Pricing and retention strategy |

| CAC | Cost to acquire each customer | Marketing budget allocation |

| LTV:CAC ratio | Acquisition efficiency | Assessing growth sustainability |

Revenue and profit tell you about the past. Enterprise value tells you what a market participant would pay for the future. That distinction shapes how you present your business to investors, lenders, or potential buyers. True business success is best measured by year-on-year change in total business value, not by any single financial statement line.

The payback period adds another layer. A business with a 3:1 LTV:CAC ratio but an 18-month payback period may struggle with cash flow even though the ratio looks healthy. A business with a 2.5:1 ratio and a 4-month payback period may actually be in a stronger position day to day. For cash-constrained businesses, the payback period is the value number that deserves the most attention.

Keeping CAC 30–50% below your break-even point based on margin and LTV creates a buffer that absorbs rising acquisition costs without destroying profitability.

Putting value numbers to work

Understanding the theory is one thing. Using these numbers to make better decisions is where the real payoff is.

- Set benchmarks for your sector. Generic benchmarks are a starting point. Industry-specific data, sourced from trade bodies or recent comparable deals, will give you far more relevant reference points.

- Review LTV and CAC quarterly. Markets shift, ad platforms change, and customer behaviour evolves. Metrics you calculated 12 months ago may no longer reflect reality.

- Improve retention before scaling acquisition. Increasing average customer lifespan by even six months can lift LTV substantially. That improvement flows directly into your LTV:CAC ratio without spending an extra pound.

- Redirect budget to efficient channels. Once you know which channels produce the lowest CAC alongside the highest LTV, concentrate spend there. Spreading budget thinly across many channels rarely produces the best results.

- Build a credible picture for investors. Investors and buyers want to see that you understand your own metrics. Presenting a clean, normalised enterprise value alongside a well-evidenced LTV:CAC ratio communicates confidence and competence.

Investing in the right professional contact number for your business may seem unrelated to these calculations, but brand touchpoints directly influence customer conversion rates and, by extension, your effective CAC.

My take on value numbers in practice

I have watched business owners obsess over revenue for years, treating it as their headline achievement. I understand the instinct. Revenue is visible, shareable, and feels like proof of momentum. But in my experience, focusing on revenue without understanding enterprise value creates a blind spot that catches people out when they try to raise funding or sell.

The most common CAC error I see is treating ad spend as the whole story. People run the numbers, feel reassured, and then wonder why the business is not as profitable as the metrics suggest. When you add in team time, software, and agency retainers, the true CAC is often 40–60% higher than the ad spend figure alone. That changes everything about how you assess a channel.

What genuinely transformed the thinking of several business owners I have spoken with was factoring in payback period. A ratio alone tells you about efficiency. Payback period tells you about survivability. Those two things are not the same.

My honest advice: treat your value numbers as a system, not a scoreboard. No single figure tells the full story. The owners who make the best decisions are the ones who hold three or four key metrics in mind simultaneously and understand how they relate to each other. Chase one number in isolation and you will optimise for the wrong outcome.

— Rob

Boost your business value with the right number

Your value numbers tell the story of your business. Your phone number tells customers who you are before they even speak to you.

At Phonenumbers, we provide memorable UK landline and mobile numbers, including 01, 02, and 07 prefixes, that strengthen brand recognition and build trust from first contact. A memorable number is not just a communication tool. It reduces friction in the customer journey, which translates directly into lower effective CAC and better conversion rates. When your acquisition strategy depends on every touchpoint performing, a bespoke phone number earns its place in your marketing stack. Browse the full catalogue and find your business number today.

FAQ

What is a value number for business?

A value number for business is a financial metric used to estimate what a business is worth. It can refer to enterprise value, equity value, or customer acquisition metrics such as LTV and CAC, depending on the context.

How do you calculate business value?

The most common approach is to normalise your earnings (adjusted EBITDA), apply an industry-relevant multiple, then subtract debt and add surplus cash to arrive at equity value. Internal calculations can come within 20–30% of a formal appraisal.

What is a good LTV:CAC ratio?

A ratio of 3:1 is the widely accepted benchmark for 2026, meaning you earn £3 for every £1 spent on acquisition. A ratio below 1:1 indicates you are losing money on each new customer.

Why does enterprise value differ from revenue?

Revenue reflects past sales performance, while enterprise value reflects the total operational worth of the business including future earning potential. Relying on revenue alone as a value number leads to poor pricing decisions during sales or funding rounds.

How often should I review my value numbers?

Quarterly reviews are advisable for LTV and CAC, given how quickly market conditions and acquisition costs can change. Enterprise value should be revisited annually or ahead of any major financial event such as fundraising or a potential sale.